Singapore’s Private Residential Market: Stabilising Rentals and Resilient Sales in Q3 2024

Singapore’s private residential market in 2024 is navigating a dual narrative of stabilising rental prices and a robust rebound in new launches. While challenges persist, particularly in the Core Central Region (CCR) and high-end rental segments, the Rest of Central Region (RCR) and Outside Central Region (OCR) continue to underpin market resilience, supported by evolving buyer and tenant preferences.

Rental Market Dynamics

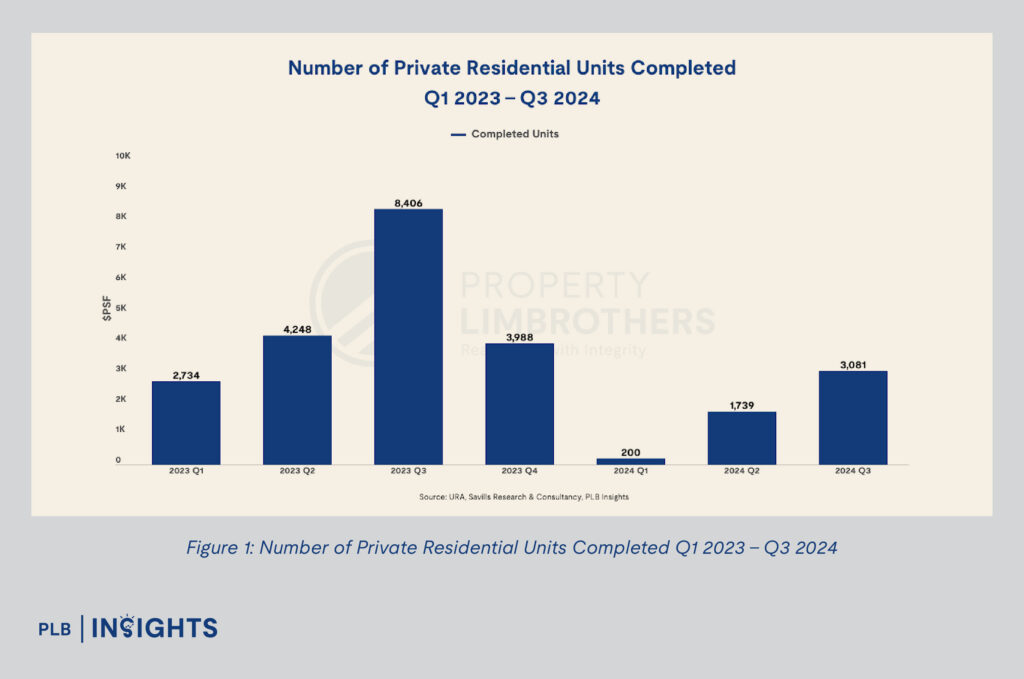

The private residential rental market is forecasted to contract by 2.5% in 2024, as the absorption of an oversupply from the previous year progresses, according to Savills report. In 2023, completions peaked at 19,376 units (excluding executive condominiums), exerting significant downward pressure on rents and driving vacancy rates higher. This situation began to stabilise in 2024, with completions slowing significantly to 200 units in Q1, 1,739 in Q2, and 3,081 in Q3, as seen in Figure 1.

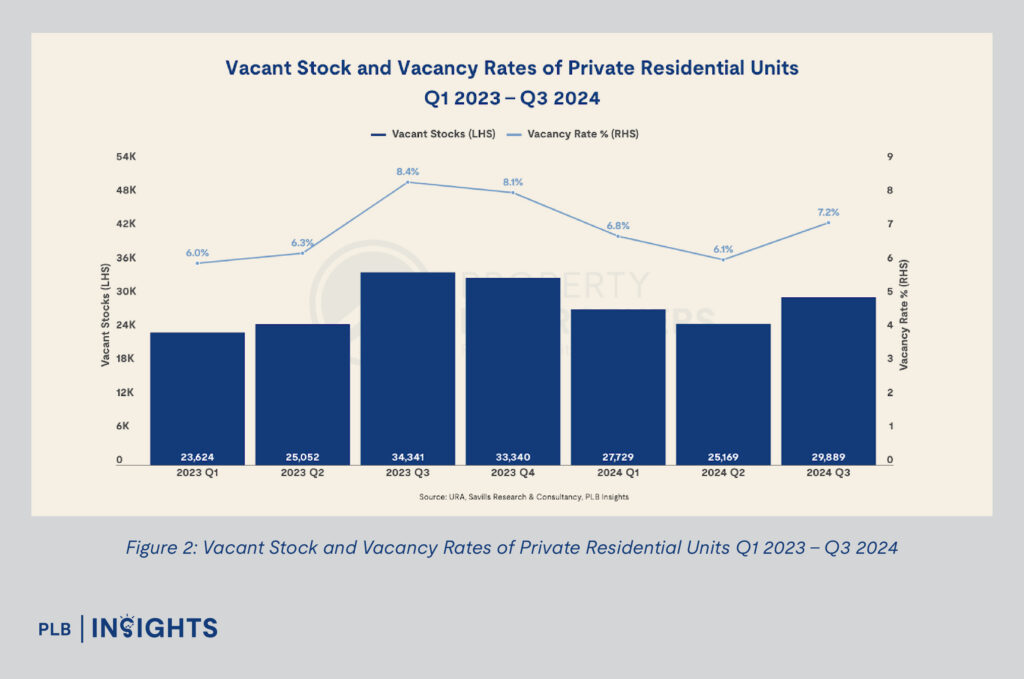

Despite the easing supply, the island-wide vacancy rate rose from 6.1% in Q2 2024 to 7.2% in Q3 2024, as seen in Figure 2. The increase was driven by a surge in vacant stock in the RCR, which grew 41.3% quarter-on-quarter (q-o-q), and the CCR, which saw a 21.2% rise. Overall, the projected annual completions of 9,100 units for 2024 signal a likely return to equilibrium in the coming quarters.

Evolving Tenant Preferences

Shifting tenant behaviours have defined the rental market in 2024. Following a year of declining rents, tenants increasingly gravitated toward one- and two-bedroom units in suburban entry-level condominiums. Seasonal demand, coupled with lower rents, catalysed this movement in Q3 2024.

Savills highlighted that 83.6% of rental contracts in projects such as Stirling Residences, Park Colonial, and Marina One Residences involved smaller units. The RCR and OCR led leasing growth, with transactions rising 25.2% and 21.2% q-o-q, respectively. In contrast, demand in the CCR lagged due to elevated vacancy rates and weaker interest from expatriates with housing allowances.

Segmented Rental Performance

The URA rental index for island-wide non-landed private homes posted a 0.5% q-o-q increase in Q3 2024, reversing three consecutive quarters of decline. The RCR and OCR led this recovery, recording growth of 1.7% and 2.2%, respectively. Seasonal factors such as corporate relocations, lease renewals, and a decentralisation trend in the commercial sector along with an expanding pool of entry-level condominiums, supported this resurgence.

However, the CCR continued to struggle, with a 1.6% drop in rents marking its fifth straight quarterly decline. High-end non-landed rents fell by 0.9% q-o-q, reflecting broader economic uncertainties and declining expatriate inflow. Since Q2 2023, high-end rents have cumulatively declined by 7.2%.

Rebound in New Launches

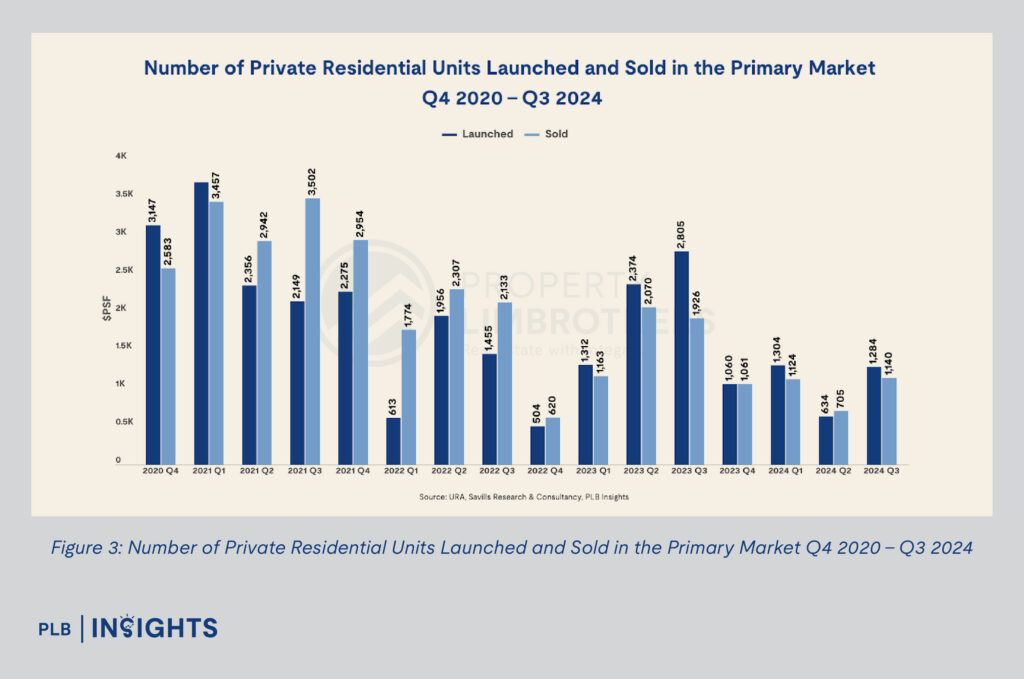

The private residential market’s recovery was evident in the rebound of new launches in Q3 2024. The number of units launched more than doubled from 634 units in Q2 to 1,284 units in Q3. The surge was primarily driven by the RCR and OCR, which contributed 36.4% and 60.9% of new launches, respectively. While the RCR saw its launches nearly double, the OCR experienced a sixfold increase.

In contrast, the CCR continued to lag, with launched units plummeting 86.9% q-o-q to just 34 units, highlighting the impact of cooling measures and diminished foreign buyer interest.

Resilient Sales Performance

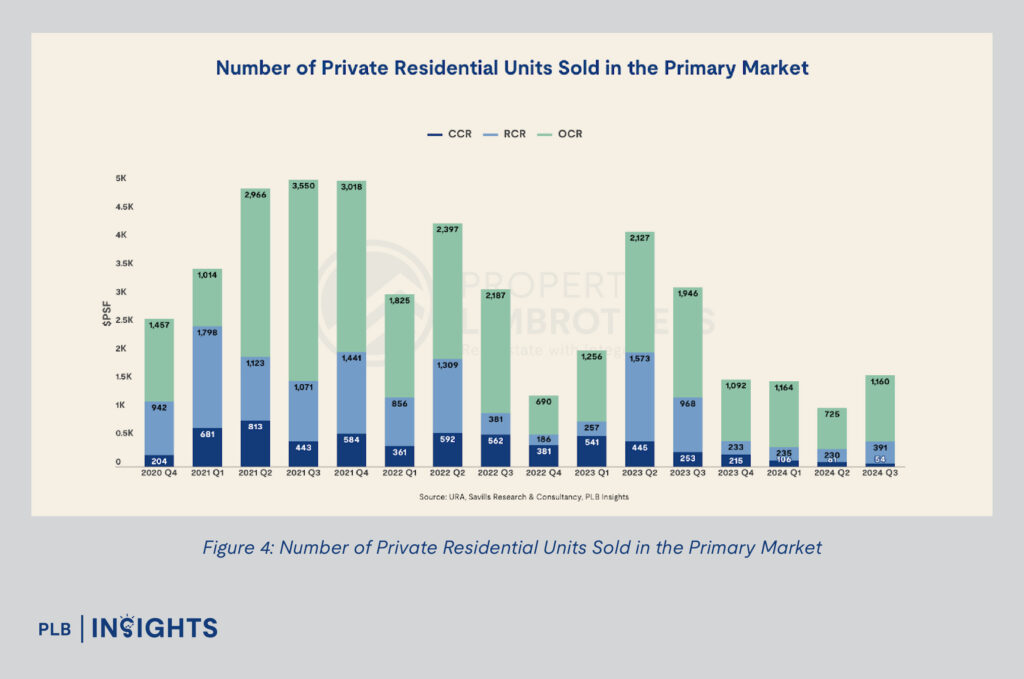

New sales expanded by 60% q-o-q to 1,160 units in Q3 2024, driven by strong performances in the RCR and OCR, as seen in Figure 4. These regions recorded sales increases of 70% and 72.7%, respectively.

Key projects such as Kassia and 8@BT saw robust demand. Kassia, a freehold development in Flora Drive, sold 59.4% of its 276 units during Q3, with pricing below S$1.5 million for most units. Similarly, 8@BT, strategically located near Beauty World MRT, achieved a take-up rate of 51.3%. The OCR also stood out as new sales surpassed launches for the second consecutive quarter.

Conversely, the CCR saw just 54 units sold—its sixth consecutive quarterly decline. New sales in the CCR accounted for only 4.7% of total transactions in Q3 2024, reflecting continued challenges posed by higher Additional Buyer’s Stamp Duty (ABSD) rates and waning foreign buyer interest.

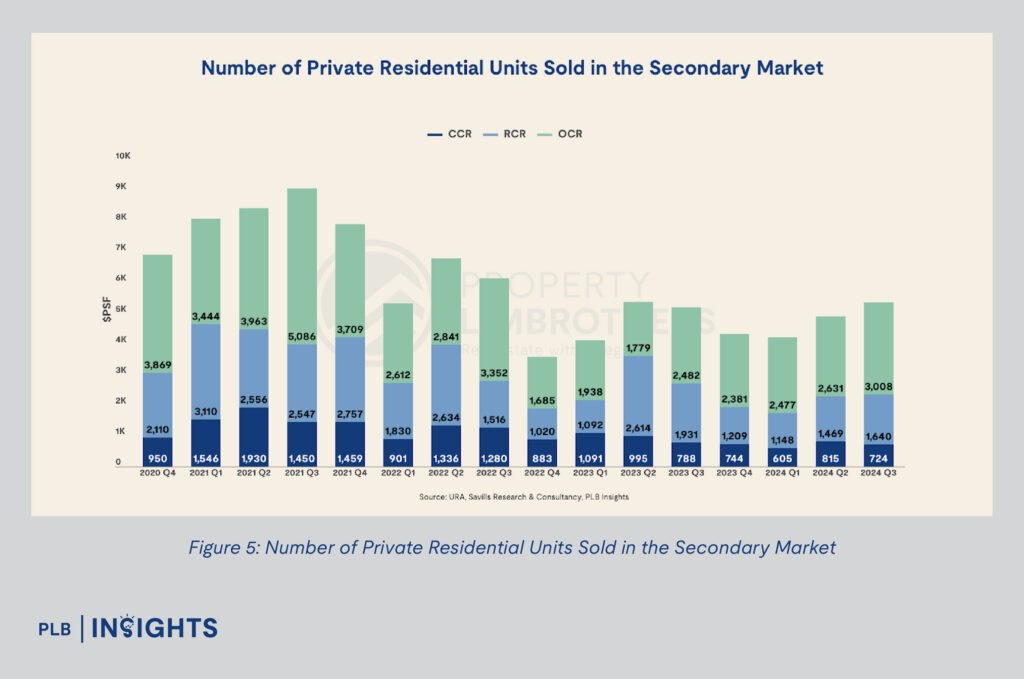

Secondary Market Trends

Secondary market transactions grew for the second consecutive quarter, rising by 0.5% q-o-q to 4,212 units in Q3 2024, as seen in Figure 5. The RCR and OCR contributed to this growth, with sales up by 0.8% and 3.4%, respectively. Despite an 8.7% q-o-q decline, CCR secondary sales remained 25.2% higher year-on-year, highlighting pockets of resilience.

Local buyers continued to dominate the market, with Singaporean purchases accounting for 81.3% of non-landed residential sales in Q3 2024. In contrast, purchases by Permanent Residents (PRs) and foreigners declined, reflecting the impact of stringent cooling measures.

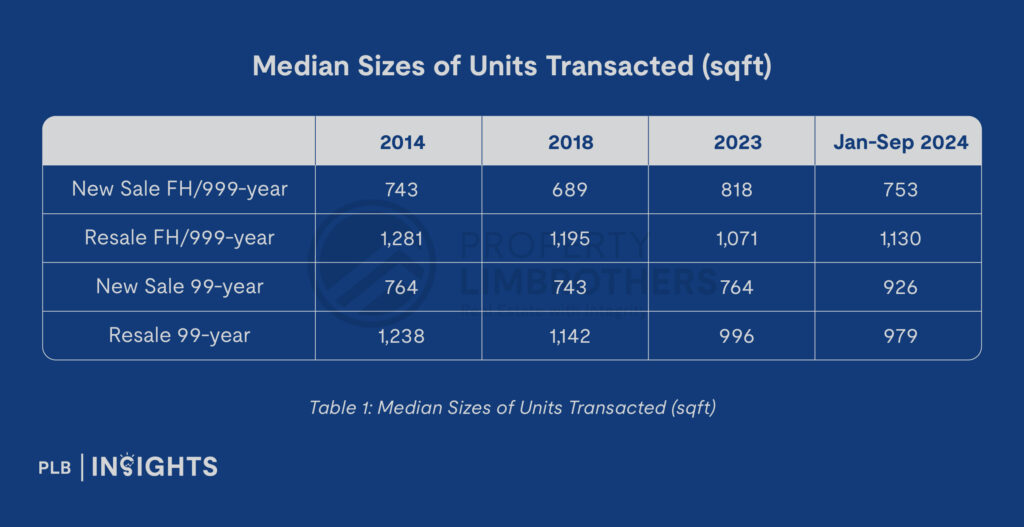

Emerging Trends: Demand for Larger Units

Median Sizes of Units Transacted (sqft)

In 2024, buyer preferences showed a noticeable shift toward larger units. The median size of units sold in 99-year leasehold developments increased to 926 square feet, up from 764 square feet in 2023. This growth in median unit size may be attributed to the significant rise in HDB resale prices, which climbed by 39.5%. By comparison, median new sale prices for non-landed properties in the RCR and OCR grew by 28.3% and 29.2%, respectively. The narrowing price gap between the public housing and private property markets is likely encouraging HDB upgraders to purchase new private properties for their own use.

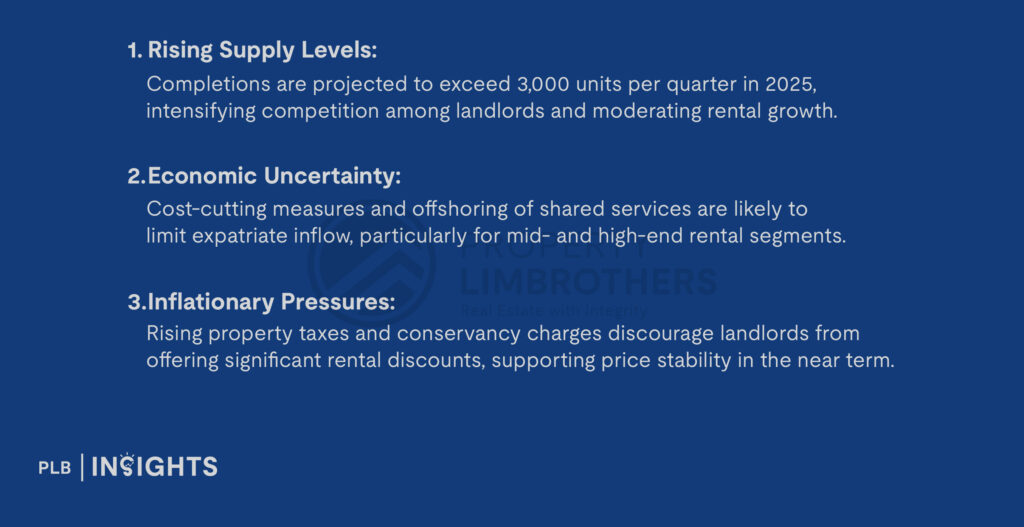

Challenges and Opportunities

While the market shows signs of recovery, challenges persist:

Outlook for 2025

Private residential rents are expected to stabilise in 2025, with the RCR and OCR likely to drive growth due to resilient local demand and strategic pricing. Developers and landlords must adapt to evolving tenant preferences, focusing on affordability, value, and larger unit layouts.

The CCR may continue to face headwinds, with any recovery in the high-end segment dependent on global economic conditions and expatriate hiring trends.

Conclusion

Singapore’s private residential market in 2024 is characterised by a delicate balance between stabilising rentals and resilient sales activity. While the CCR faces ongoing challenges, the RCR and OCR provide bright spots, buoyed by local demand and strategic pricing. As developers and landlords adjust to these dynamics, the market is well-positioned for steady growth in 2025, supported by its adaptability and resilience amidst broader uncertainties.

For more detailed Q3 2024 analysis, do keep a lookout for our upcoming Q3 2024 Report on PLB Insights!

Let’s Get In Touch

Our goal is to provide you with the latest market updates and assist you with any questions that you have. Don’t hesitate to reach out to us and our team of experienced consultants will be ready to assist with a personalised consultation.

Disclaimer: Information provided on this website is general in nature and does not constitute financial advice

PropertyLimBrothers will endeavour to update the website as needed. However, information may change without notice and we do not guarantee the accuracy of information on the website, including information provided by third parties, at any particular time. While every effort has been made that the information provided is accurate, individuals must not rely on this information to make a financial or investment decision. Before making any, we recommend you consult a financial planner or your bank to take into account your particular financial situation and individual needs. PropertyLimBrothers does not give any warranty as to the accuracy, reliability or completeness of information which is contained in this website. Except insofar as any liability under statute cannot be executed, PropertyLimBrothers, its employees do not accept any liability for any error or omission on this website or for any resulting loss or damage suffered by the recipient or any other person.