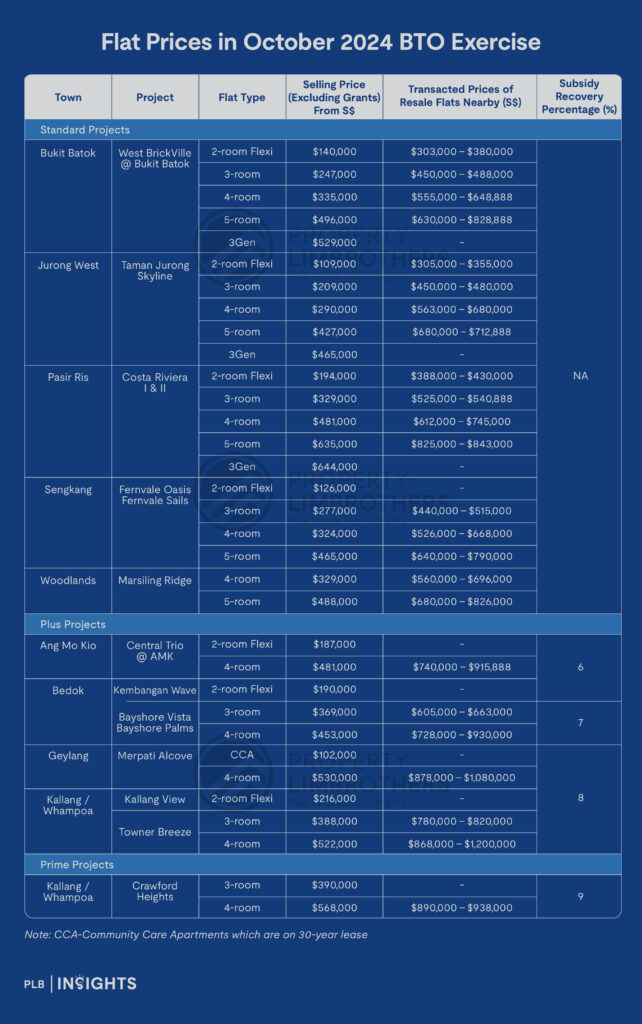

October 2024 saw the launch of 15 projects in nine estates across Singapore. In two previous articles, we explored these sites in detail. The first article covered Ang Mo Kio, Bedok, Bukit Batok, and Geylang, while the second focused on Jurong West, Kallang/Whampoa, Pasir Ris, Sengkang, and Woodlands. The launch coincided with the introduction of the new HDB classification framework, which also incorporates subsidy clawbacks (upon future resale).

Under this framework, the subsidy clawback for Plus flats will range from 6% to 8%, depending on the location. For the sole Prime flat, the subsidy clawback will be 9% if the owner decides to sell after meeting the 10-year Minimum Occupation Period (MOP).

Additional subsidies are offered to BTO buyers in more desirable locations (Plus and Prime flats) to ensure affordability. However, to prevent speculative buying and ensure HDB flats remain homes for Singaporeans rather than profit-driven assets, the subsidy clawback mechanism was introduced. Properties in prime locations, whether public or private, generally command higher prices. In recent years, especially post-pandemic, some resale HDB flats in sought-after areas have sold for over a million dollars, with one 5-room flat nearing the $2 million mark earlier this year.

Without the clawback mechanism, owners of Plus and Prime flats, who initially benefit from subsidies, could make large profits when selling in the resale market. Additionally, without income ceiling restrictions for resale buyers of these flats, sellers could set high asking prices, further driving up resale HDB prices overall.

In this article, we’ll explore the key considerations when choosing between a Standard, Plus, or Prime flat, with fictional case studies to make these distinctions clearer.

Subsidy Clawbacks For October 2024’s BTO Launch Exercise

Among the Plus category flats, Kembangan Wave and Central Trio @ AMK will have a 6% subsidy clawback. Bayshore Vista and Bayshore Palms, due to their better locations near East Coast Park, will face a 7% clawback when sold after the 10-year Minimum Occupation Period (MOP). Two Kallang/Whampoa projects—Kallang View and Towner Breeze—will have an 8% clawback. Meanwhile, the sole Prime project, Crawford Heights, will come with a 9% clawback when resold on the open market after the MOP.

Comparing Standard, Plus, and Prime Flats: Real Estate Journeys of Three Couples

In this case study, we examine the potential real estate journeys of three couples, each choosing a different type of flat: Standard, Plus, and Prime.

To ensure consistent projections, we assume consistent household incomes, loan tenures and construction years across all scenarios:

- All couples are 30 years old with a combined monthly income of $7,000, which is expected to double to $14,000 in five years, after securing their flat.

- All couples will also take a 25-year HDB loan

- construction of all flats will take five years. Each couple applies for a 4-room BTO flat.

We estimate a Compounded Annual Growth Rate (CAGR) of 3.75% for the Standard flat, compared to 2.51% for the Plus and Prime flats, reflecting recent HDB price trends over the years. Compounded Annual Growth Rate, shows how much an investment grows on average each year, taking into account the effect of compounding.

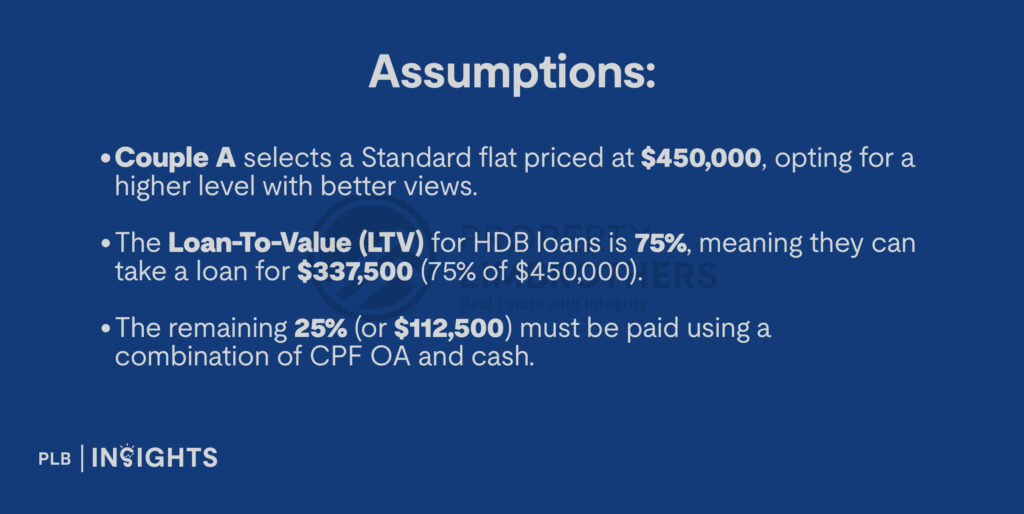

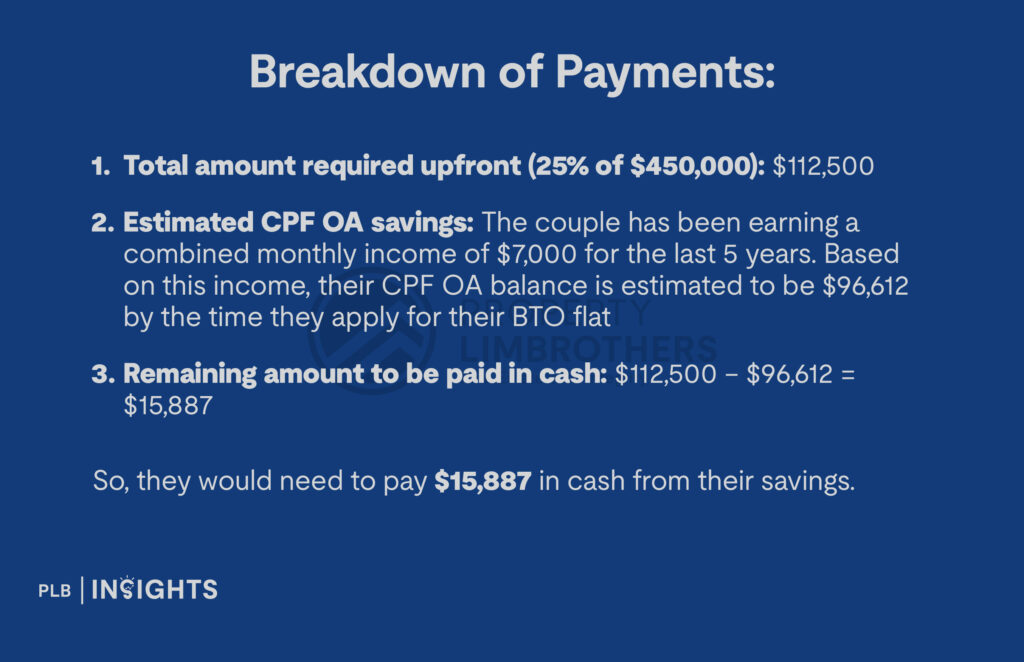

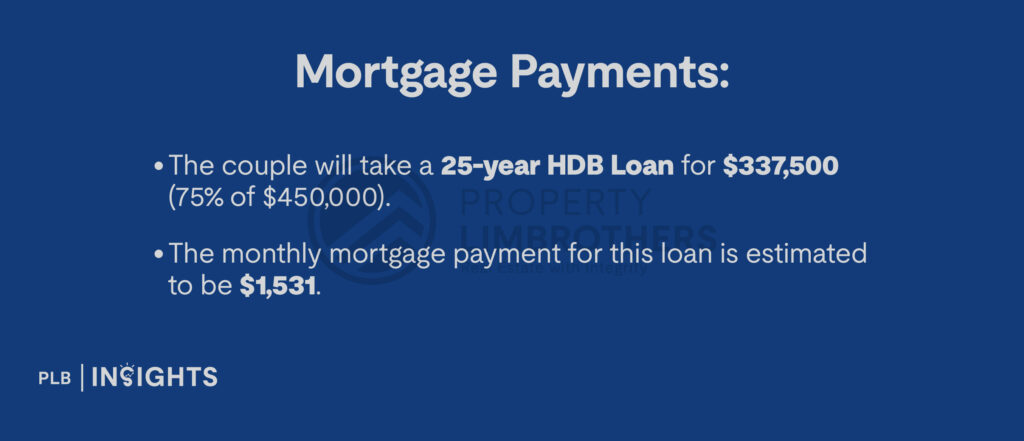

Scenario A: Couple A Who Opts For A Standard Flat

Can the mortgage be fully covered by CPF?

Yes, with their monthly CPF OA contribution of $3,220 exceeding the mortgage payment of $1,531, the couple can fully cover their mortgage using CPF, without needing to pay cash. This frees up the rest of their monthly income, allowing them to save or invest in revenue-generating assets, which will significantly support their future plans for upgrading.

Selling Off the Flat After MOP

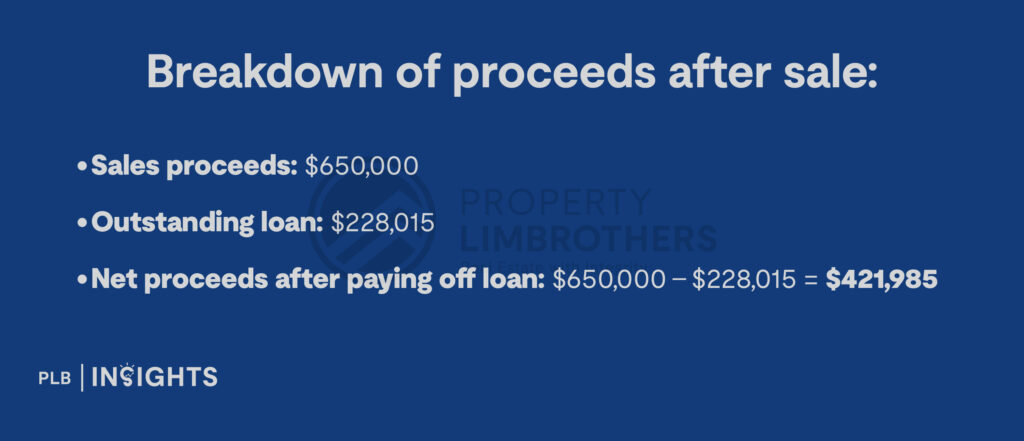

Assuming they sell their Standard flat for $650,000 after fulfilling the MOP, reflecting a 45% capital appreciation, this would result in a $200,000 gain (excluding any sale-related costs). At the time of sale, they would still owe approximately $228,015 on their HDB loan.

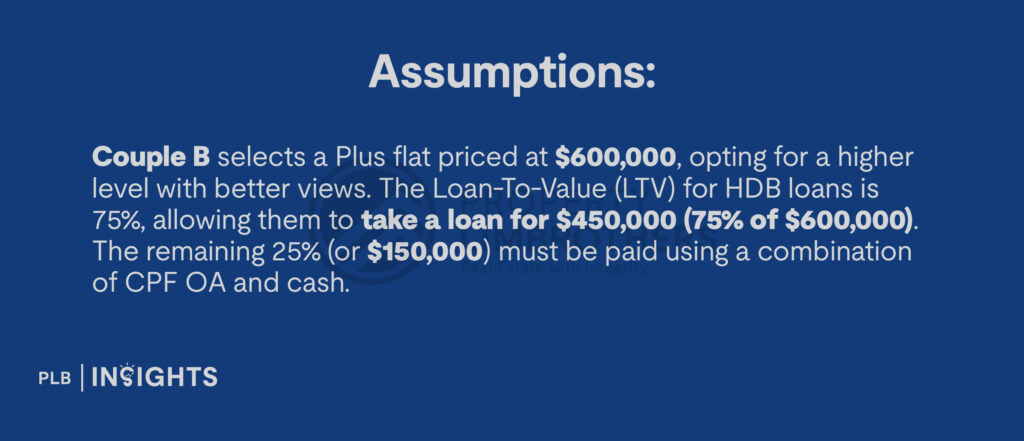

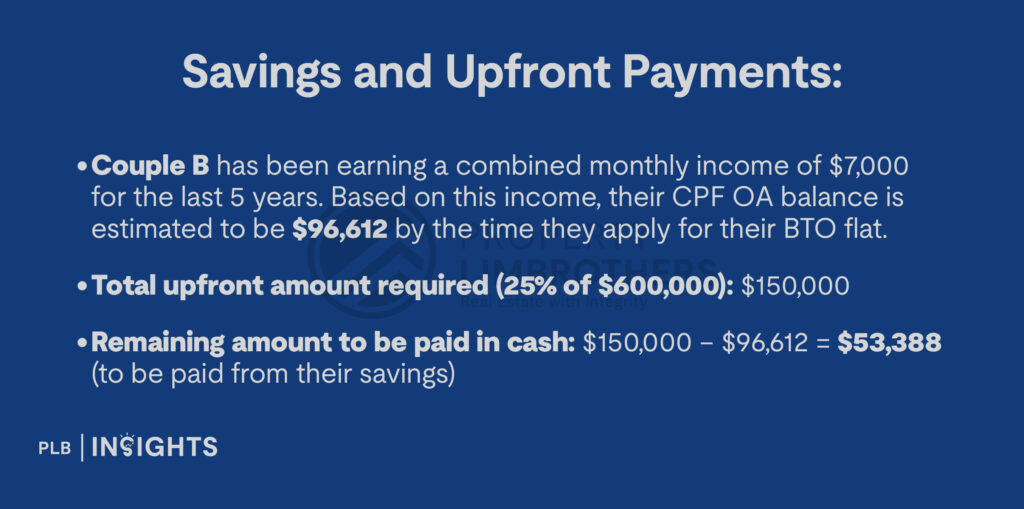

Scenario B: Couple B Who Opts for a Plus Flat

Can the mortgage be fully covered by CPF?

Yes, with their CPF OA contribution of $3,220 exceeding the monthly mortgage payment of $2,042, the couple can fully cover the mortgage using CPF, leaving their cash flow intact for other savings or investments.

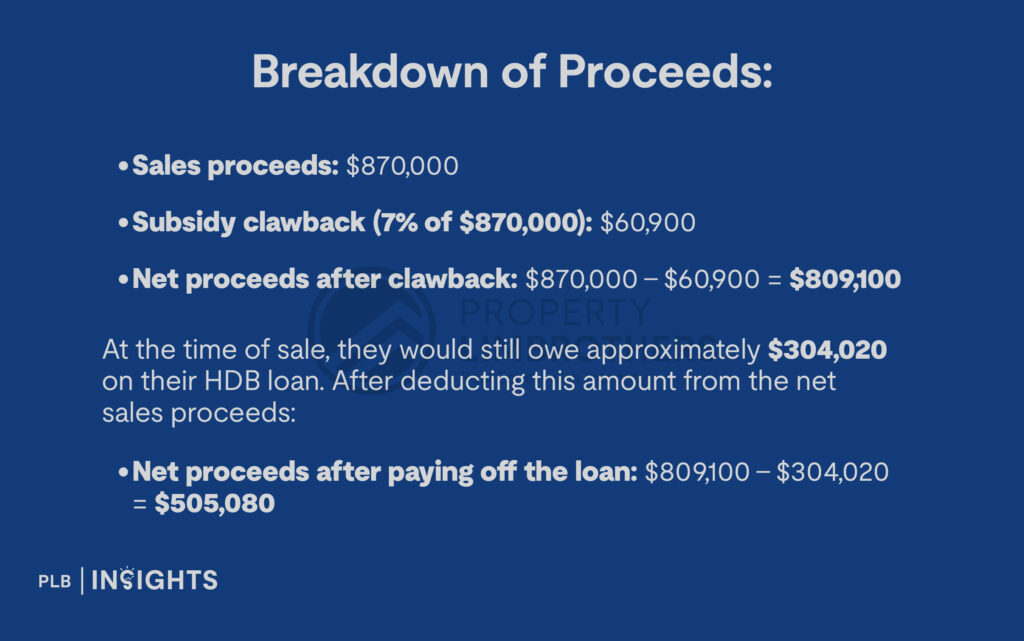

Selling Off the Flat After MOP (Including 7% Subsidy Clawback)

Assuming they sell their Plus flat for $870,000 after fulfilling the 10-year MOP, the first deduction they will face is the 7% subsidy clawback, amounting to $60,900 of the sale price.

Caveat

While a Plus flat may offer slightly higher capital appreciation than a Standard flat in this scenario, the difference over the additional 5-year period is relatively modest. Moreover, the higher upfront cash outlay can pose a significant financial strain for a couple early in their careers. Delaying an upgrade by 10 years also means forgoing an earlier opportunity to capitalise on property appreciation. Had they upgraded 5 years earlier, they could have potentially benefited from more capital growth. The higher purchase price of a Plus flat, combined with missed opportunities for wealth accumulation, could be considerable. Furthermore, by the time Couple B reaches the end of the 10-year MOP at age 45, upgrading to a larger home or private property may no longer align with their evolving lifestyle or long-term objectives.

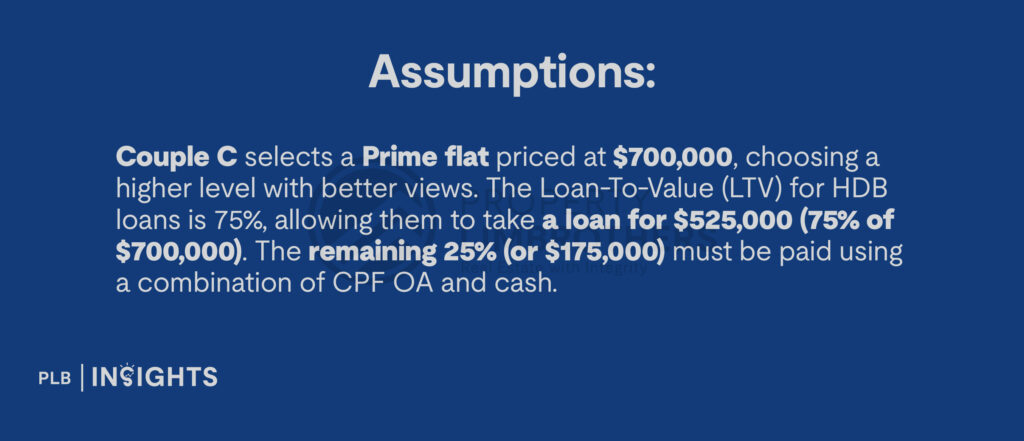

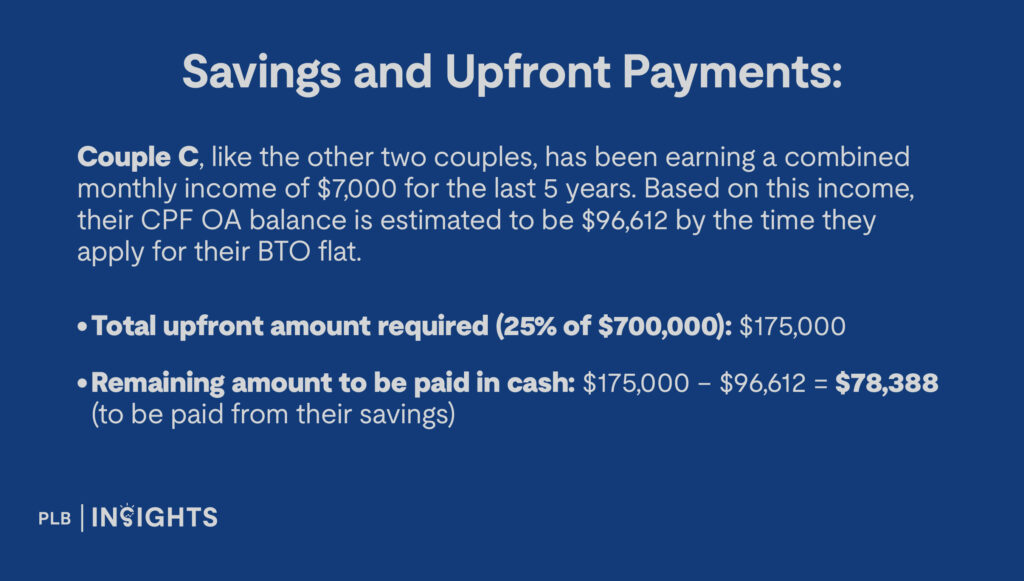

Scenario C: Couple C Who Opts for a Prime Flat

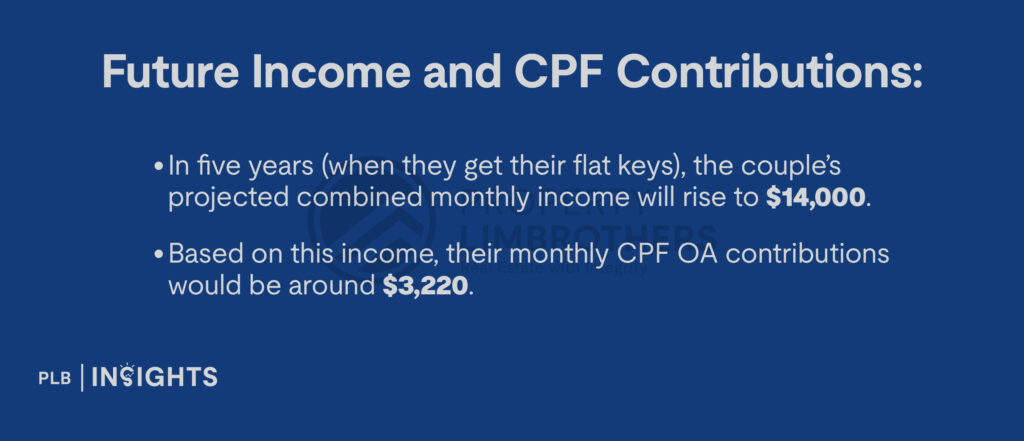

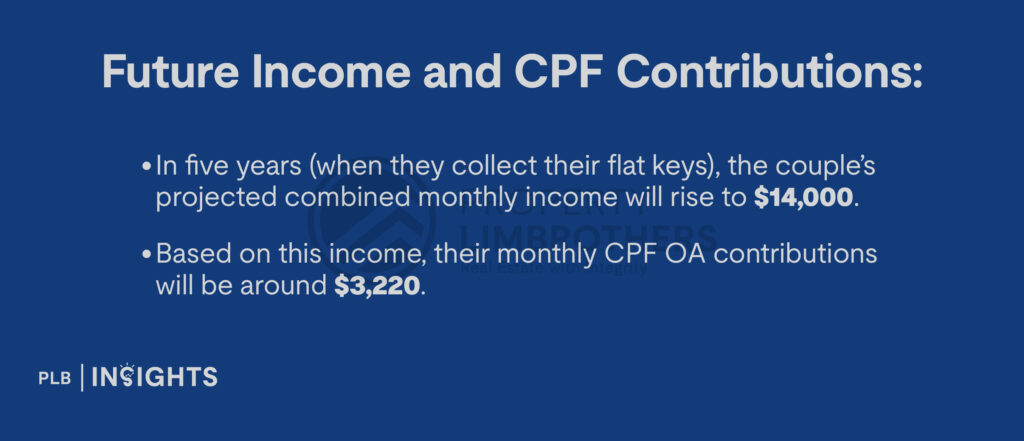

Future Income and CPF Contributions

In five years (when they collect their flat keys), the couple’s projected combined monthly income will rise to $14,000. Based on this income, their monthly CPF OA contributions will be around $3,220.

Can the mortgage be fully covered by CPF?

Yes, with their CPF OA contribution of $3,220 exceeding the monthly mortgage payment of $2,382, the couple can fully cover the mortgage using CPF, allowing them to keep their cash flow intact for other savings or investments.

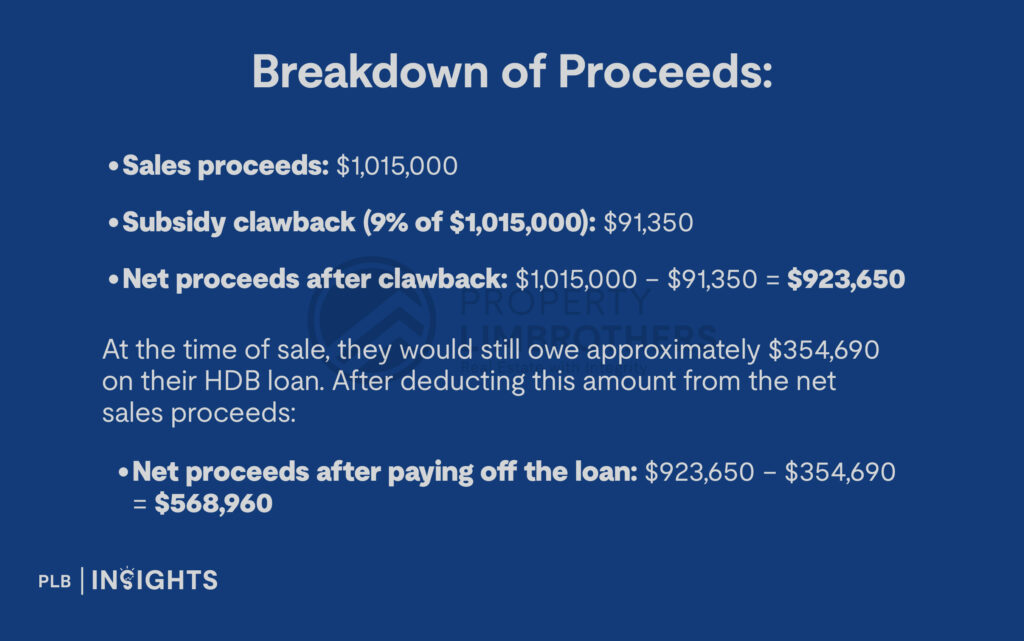

Selling Off the Flat After MOP (Including 9% Subsidy Clawback)

Assuming they sell their Prime flat for $1,015,000 after fulfilling the 10-year MOP, the first deduction they will face is the 9% subsidy clawback, amounting to $91,350 of the sale price.

Caveat

Although a Prime flat offers the highest potential for capital appreciation, it comes with the largest upfront cash outlay, which can create financial strain for a couple early in their careers. Like the Plus flat, the 10-year MOP delays the opportunity to upgrade sooner and build wealth earlier. By the time the MOP ends, at age 45, upgrading to a larger home or private property may no longer suit their lifestyle or long-term plans. Additionally, the 9% subsidy clawback, along with the higher purchase price, further reduces their overall net gains.

In Conclusion

When deciding between a Standard, Plus, or Prime flat, it’s important to consider not just the financial aspects but also how each option aligns with long-term goals and lifestyle aspirations. While Plus and Prime flats may offer higher potential capital appreciation due to their desirable locations, the difference in appreciation compared to Standard flats is not substantial given the additional 5-year MOP for Plus and Prime flats. Thorough consideration must be given to whether the longer MOP and higher upfront costs are worth the delayed opportunity for an upgrade.

Ultimately, the decision should be based on a balance between affordability, future flexibility, and alignment with personal goals. Buyers must carefully evaluate whether the higher purchase price and subsidy clawbacks in Plus and Prime flats justify the potential capital gains, while ensuring their choice supports their broader aspirations in the long run.

If you are weighing your options in the market and would like a second opinion, do contact us here and our team of experienced consultant will be glad to help break down your financial calculations and explore your options.